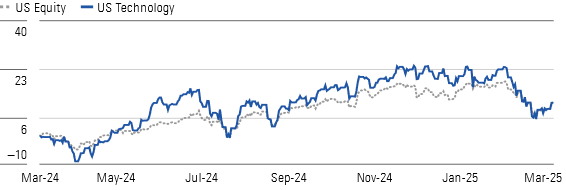

After good performances throughout 2024, the technology sector collapsed in the first quarter of 2025. Although we recently thought that the sector was quite appreciated overall, we now consider it attractive. The results of the software companies were generally solid, but the actions worked hard in the previous quarter and now return to levels consistent with the start of this performance.

Overall, Tech was the second most awakening sector in the first quarter, which led to its performance, to be one of the most efficient sectors in the last 12 months in the middle of the pack. We do not see any coherent differentiation of performance among market capitalization sections. Our confidence in secular winds, such as cloud computing, artificial intelligence and long-term expansion of semiconductor demand, remains unchanged. As technological actions have sold, we see increased investment opportunities. THE US morningstar technology index Increased 11.4% on a train-around-12 month, compared to the American equity market up 11.5%. During the quarter, the American equity market fell 1.74%, while technology fell 7%.

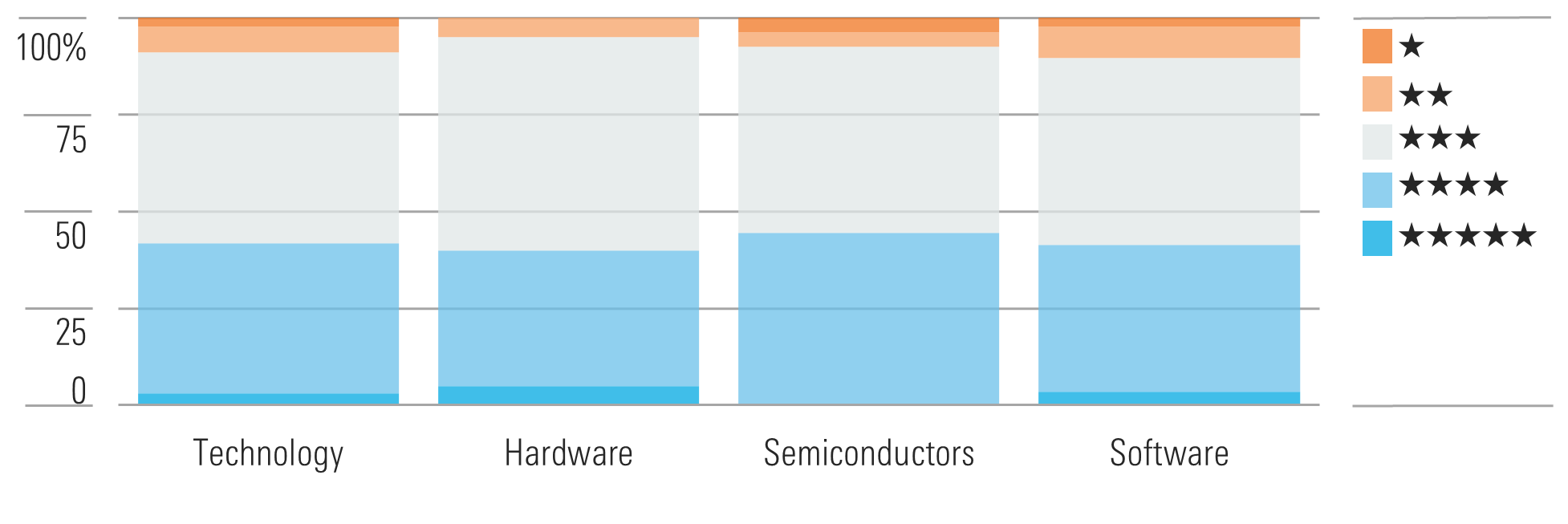

The median American technology stock is undervalued, with a reasonable safety margin. We consider the hardware as the most undervalued, the semi-finals and the software are also attractive.

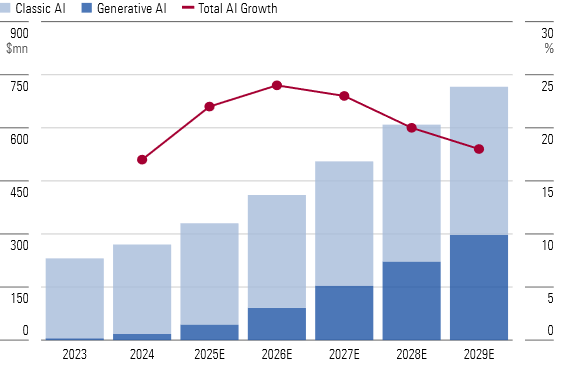

The generative AI remains the largest theme in the technological sector. Software companies develop and incorporate new generation AI capabilities into their solutions, while cloud suppliers introduce new services and ramp capacities, and certain semiconductor companies, including NVIDIA, undergo an increasing demand for AI and data center demand. That said, the actions of companies related to AI also sold at the beginning of 2025.

We believe that generative AI will support income growth over the next five years, even if it has not led to a lot of growth in the past year or two, buyers have mainly evaluated technology. Growth has certainly been explosive for public cloud sellers. We note the largest cases of generative use of AI in the coming years in the fields of customer service and software. The two markets are already important and the effectiveness drawn from the generative AI makes it a convincing value proposal.

Main choices of technology sector

NXP semiconductors

NXP semiconductors Nxpi is one of our best choices in the analog and mixed chip space. We particularly like the disproportionate exposure of the company to the final automotive market, where it obtains almost 50% of income. NXP is well diversified as an automobile, with a nice portfolio of processor products, microcontrollers and analog parts. We believe that the company will also gain its fair share in electrified and safety automobile products, such as radar management systems and batteries. Overall, NXP automotive activities are linked to secular winds in the increase in flea markets per vehicle, and we believe that the market is too focused on short -term slowdown in demand. We expect NXP to return to income growth in 2025.

Adobe

Adobe Adbe came to dominate in the content creation software with its emblematic Photoshop and Illustrator solutions, which are both contained in the wider creative cloud, which is the clear software leader for creation professionals. Adobe Express widens the funnel for new customers, which, in our view, is increasing well for growth in the coming years. We also consider that generative fireplace models as an important growth engine. Overall, we see a lot of momentum in product innovation, customer interest and income creation, and we are encouraged by solid quarterly results

Microsoft

Microsoft Msft Dominates several of its markets served, as with Office In Productivity Software and Windows for PC operating systems, and it has been established as one of the clear leaders in the public cloud. We believe that the proliferation of hybrid cloud environments will continue to strengthen its position with Azure. In addition, the company’s investment in Openai has catapulted Microsoft to a management position in a generative AI, which has motivated an acceleration of the growth of Azure during the recent quarters.